Most jurisdiction comparisons are written by firms that only operate in one country — which makes the analysis predictably one-sided. This guide is different. Affinitas Advisory is based in Dubai and the UAE is our home market.

The Three Jurisdictions at a Glance

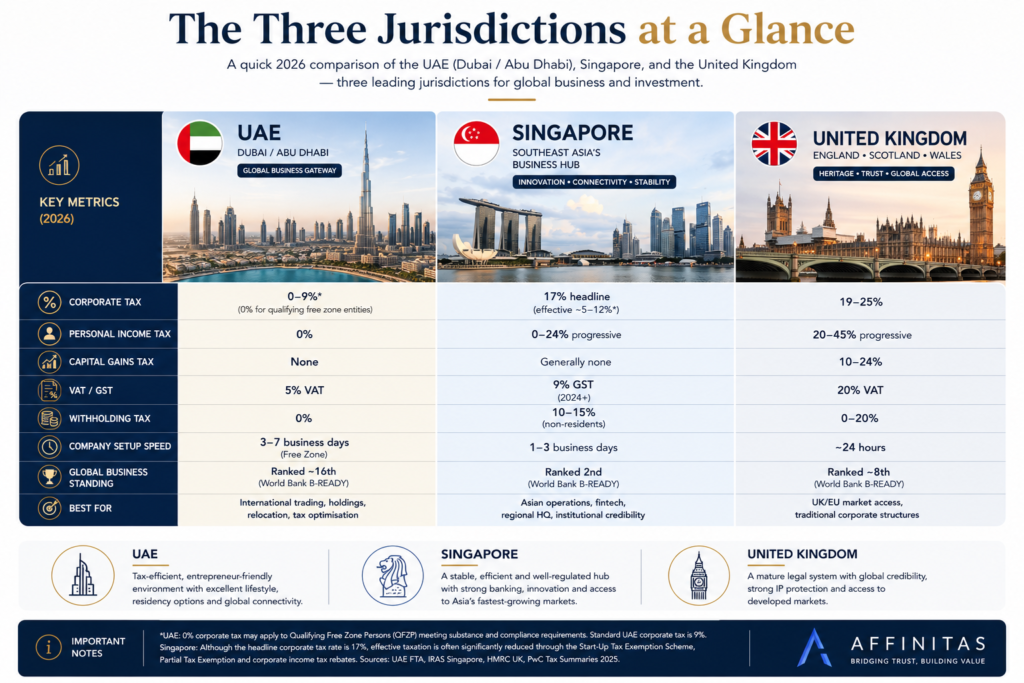

When international founders and investors evaluate where to establish a company, the conversation consistently narrows to three leading jurisdictions: the UAE (particularly Dubai), Singapore, and the United Kingdom. Each has become a global business hub for different strategic reasons — whether tax efficiency, banking access, international credibility, or operational simplicity.

The key mistake many entrepreneurs make is assuming one jurisdiction is universally “better.” In reality, the optimal structure depends on several factors: your industry, client geography, expected profit levels, long-term residency plans, and future exit strategy.

Below is a simplified 2026 comparison of the three most frequently selected jurisdictions for international business setup and holding structures.

| Category | 🇦🇪 UAE (Dubai / Abu Dhabi) | 🇸🇬 Singapore | 🇬🇧 United Kingdom |

|---|---|---|---|

| Corporate Tax | 0–9%* | 17% headline (effective ~5–12%*) | 19–25% |

| Personal Income Tax | 0% | 0–24% progressive | 20–45% progressive |

| Capital Gains Tax | None | Generally none | 10–24% |

| VAT / GST | 5% VAT | 9% GST | 20% VAT |

| Withholding Tax | 0% | 10–15% (non-residents) | 0–20% |

| Company Setup Speed | 3–7 business days | 1–3 business days | ~24 hours |

| Business Reputation | Fast-growing global hub | Strong Asian financial centre | Long-established global credibility |

| Best For | International trading, holdings, relocation, tax optimisation | Asian operations, fintech, institutional credibility | UK/EU market access, traditional corporate structures |

| Banking Environment | Improving rapidly, relationship-based | Extremely strong and stable | Mature but increasingly compliance-heavy |

| Regulatory Style | Pro-business, evolving | Structured and highly efficient | Mature but more bureaucratic |

| Global Business Standing | ~Top 20 globally | ~Top 2 globally | ~Top 10 globally |

Important Notes

* UAE: 0% corporate tax may apply to Qualifying Free Zone Persons (QFZP) meeting substance and compliance requirements. Standard UAE corporate tax is 9%.

* Singapore: Although the headline corporate tax rate is 17%, effective taxation is often significantly reduced through the Start-Up Tax Exemption Scheme, Partial Tax Exemption, and corporate income tax rebates.

Strategic Positioning in 2026

- The UAE remains one of the most attractive jurisdictions for founders seeking tax efficiency, residency options, operational flexibility, and international structuring opportunities.

- Singapore continues to dominate as Asia’s premium jurisdiction for fintech, regional headquarters, and institutional-grade business credibility.

- The United Kingdom still offers strong international recognition and legal stability, particularly for companies serving UK or European clients, despite higher tax exposure.

The “best” jurisdiction is ultimately the one that aligns with your operational reality, tax residency position, banking needs, and long-term expansion strategy — not simply the lowest headline tax rate.

The Number That Changes Everything: Personal Income Tax

For founders, directors, and high-earning professionals, the corporate tax rate matters — but the personal tax rate on what they ultimately take home is often the larger number. This table illustrates the real-world difference for an individual earning the equivalent of USD $200,000 annually across all three jurisdictions. Figures are approximations based on 2025/26 standard rates and do not account for all reliefs or deductions.

| Jurisdiction | Gross Income (USD) | Est. Personal Tax | Net Take-Home (USD) | Annual Tax Cost (USD) |

|---|---|---|---|---|

| 🇦🇪 UAE (Dubai) | $200,000 | 0% | $200,000 | $0 |

| 🇸🇬 Singapore | $200,000 | ~15–17% | ~$166,000–$170,000 | ~$30,000–$34,000 |

| 🇬🇧 UK (England) | $200,000 | ~45%+ | ~$108,000–$115,000 | ~$85,000–$92,000 |

Figures are indicative estimates based on 2025/26 headline rates. Singapore tax at these income levels approx 15–17% effective (progressive 0–24% schedule, first SGD 20,000 tax-free). UK figure includes 45% additional rate on income above £125,140, National Insurance contributions, and dividend tax at revised rates from April 2026.

Sources: IRAS, HMRC, UAE FTA. Seek jurisdiction-specific professional advice for your personal position.

For a high-earning professional relocating from the UK to the UAE, this represents a potential difference of $85,000–$92,000 per year in retained income. Compounded over ten years, with that capital invested rather than paid in tax, the wealth differential is transformative. This is not a marginal optimisation — it is a structural shift in wealth accumulation velocity.

"Tax is not the only variable in a relocation or incorporation decision. But for high earners and founders, it is the variable that compounds most aggressively over time. Getting it right at year one matters more than most people appreciate until they look back at year ten."— Affinitas Advisory Team, Dubai

The Full Comparison: UAE vs Singapore vs UK Across Every Dimension

Tax rates capture attention, but they rarely capture the full picture. The following table compares all three jurisdictions across the operational, regulatory, and lifestyle factors that sophisticated founders weigh before committing.

| Factor | 🇦🇪 UAE | 🇸🇬 Singapore | 🇬🇧 United Kingdom |

|---|---|---|---|

| Corporate Tax Rate | 0–9%* | 17% (eff. lower) | 19–25% |

| Personal Income Tax | 0% | 0–24% | 20–45% |

| Capital Gains Tax | None | None (generally) | 10–24% (assets, BADR applies) |

| Inheritance / Estate Tax | None | None | 40% IHT above £325k threshold |

| VAT / GST | 5% UAE VAT | 9% GST (from 2024) | 20% VAT |

| Withholding Tax (outbound) | 0% | 10–15% (non-residents) | 0–20% (varies by treaty) |

| Tax Treaty Network | 140+ treaties | 90+ treaties | 130+ treaties |

| 100% Foreign Ownership | ✓ Yes (Free Zones + Mainland post-2021) | ✓ Yes (most sectors) | ✓ Yes |

| Company Setup Speed | 3–7 days (Free Zone) | 1–3 days | 24–48 hours |

| Setup Cost (Indicative, Year 1) | AED 13K–22K+ licence | SGD 300–600 + compliance | £12–50 Companies House |

| Legal System | UAE Civil Law (DIFC/ADGM: English Common Law) | English Common Law | English Common Law |

| Banking Access (International) | Good — improving; KYC intensive | Excellent — global Tier 1 access | Excellent — global financial centre |

| VC / Startup Ecosystem | Strong — growing rapidly in MENA | Dominant in APAC | Europe's largest — London fintech hub |

| Regulatory Complexity | Moderate — CT/ESR/substance rules | Low — clear, digital-first IRAS | High — HMRC complexity, MTD changes |

| Residency / Visa for Founders | Golden Visa (10-year), investor visa | Employment Pass — tied to company payroll | Innovator Founder Visa — selective |

| Personal Residency Requirement | 183 days/year (or 90 days + UAE centre) | Tax residency tied to presence + control | Statutory Residence Test — complex |

| Market Access — MENA | Best in class | Limited — distance from region | Moderate — via UK-based multinationals |

| Market Access — APAC | Moderate via Singapore treaty | Best in class | Significant — via UK financial institutions |

| Global Brand / Credibility | High — rapidly improving | Very high — AAA sovereign | Very high — G7 member |

All rates as of 2025/26. UAE CT: 0% (QFZP, qualifying income) or 9% standard — subject to substance conditions. Singapore effective corporate rate substantially lower than 17% headline through exemptions. UK CT: 19% (≤£50k profits) to 25% (>£250k). Sources: UAE FTA, IRAS Singapore, HMRC UK, PwC Tax Summaries, World Bank B-READY 2025.

The Honest Truth: What the UAE Gets Wrong (That Nobody Tells You)

Here is what the UAE does not do well, and what you need to weigh before committing.

| UAE Disadvantage | What It Means in Practice | Who It Affects Most |

|---|---|---|

| High Licence & Setup Costs | Free zone annual licences start from ~AED 13,000–22,000 just for the entity. Add visas, flexi-desks, CT registration, and advisory fees — Year 1 all-in costs range AED 25,000–60,000+ for a simple setup. | Solo freelancers, early-stage founders, businesses with sub-$100K revenue |

| Complex Corporate Tax Compliance | The UAE's CT regime — introduced June 2023 — is still evolving. QFZP conditions, substance requirements, transfer pricing documentation, and ESR filings create an ongoing compliance burden that did not exist pre-2023. | Any UAE free zone entity generating revenue. All entities must register with the FTA. |

| Banking KYC Intensity | Opening a UAE corporate bank account is significantly more demanding than Singapore or UK. Source of funds, UBO declarations, and compliance reviews are thorough. Some industries face rejection or 3–6 month delays. | Fintech, crypto, iGaming, high-risk industry founders; newly incorporated entities |

| Physical Presence Required for Tax Residency | To claim UAE tax residency, individuals must spend 183+ days per year in the UAE (or 90 days with UAE as their primary economic centre). For founders who travel frequently, maintaining this is non-trivial. | Global nomads, frequent travellers, founders with operations in multiple countries |

| No Exit Tax Relief Equivalent to UK/SG | Many founders relocating from the UK or EU face exit tax obligations in their home country before UAE structures become beneficial. UAE's 0% rate only helps after clean tax residency is established. | UK founders (5-year non-domicile clawback rules), German, French, and Australian citizens |

| Limited VC Ecosystem vs Singapore/UK | Dubai's VC market is growing rapidly but is substantially smaller than Singapore for APAC-focused businesses or London for European/global fintech. Institutional investors often prefer familiar jurisdictions. | Startups seeking institutional VC, Series A+ raises from global funds |

| Sharia Succession Law (Default) | Without specific legal structuring (DIFC Will, Foundation), assets held personally in the UAE default to Sharia succession law. Non-Muslims can protect against this — but it requires proactive action. | Non-Muslim founders holding personal assets in the UAE without a DIFC Will or Foundation |

⚠️ The "0% Tax" Misrepresentation

Social media portrays Dubai as "tax-free." It is not. The UAE applies 5% VAT on most services, 9% corporate tax on taxable income above AED 375,000, and a 15% Domestic Minimum Top-Up Tax for multinationals above EUR 750M revenue. The correct description is tax-efficient— not tax-free. Anyone selling you a "completely tax-free Dubai setup" is either uninformed or misleading you.

Source: UAE Federal Tax Authority.

And in Fairness: What Singapore and the UK Get Wrong

Singapore's Real Limitations

- Personal income tax reaches 24% at higher income bands — not dramatic by Western standards, but far from zero. For high earners, the gap vs UAE is $30,000–$50,000+ per year.

- Local director requirement: Singapore law requires at least one locally resident director for all companies. For foreign founders who cannot relocate, this means appointing a nominee director — an ongoing cost and governance consideration.

- GST raised to 9% from January 2024 — up from 7%. For B2C businesses, this is a meaningful operating cost increase.

- Employment Pass rules: Founders wishing to work personally in Singapore must qualify for an Employment Pass (EP). The qualifying criteria have tightened significantly in recent years, particularly for founders without significant salary packages.

- Cost of living is high: Office rents, housing costs, and professional service fees in Singapore are among the highest in Asia. For businesses that depend on lean operations, this erodes the advantage of a lower tax rate.

The UK's Real Limitations

- 25% corporation tax (from April 2023) on profits above £250,000 — one of the highest rates in developed markets. The marginal relief band between £50,000–£250,000 creates an effective rate of 26.5%, the highest in the band.

- Personal tax burden is severe for high earners: Income above £125,140 is taxed at 45%. Add employer NI, employee NI, and dividend tax (rising to 35.75% higher rate from April 2026) and the combined personal tax burden is among the highest of any major economy.

- Making Tax Digital (MTD) compliance: New digital filing obligations under MTD for Income Tax (launching April 2026 for earnings above £50k) add meaningful administrative burden.

- Inheritance Tax: 40% IHT on estates above £325,000 (£500,000 with residence nil-rate band for main home). For founders building significant personal wealth inside a UK structure, the estate planning problem is real and significant.

- HMRC complexity: The UK tax code is one of the longest in the world. Transfer pricing, IR35, CFC rules, and constant Budget-driven changes create high accounting and legal costs.

"The UK is not a bad place to have a company — it is a highly credible, globally respected jurisdiction. It is a very bad place to pay tax as an individual high earner or to accumulate personal wealth over a generation. Those are different problems with different solutions."— Affinitas Advisory Team, Dubai

The Decision Framework: Who Should Incorporate Where?

Rather than declaring a winner, the right question is: which jurisdiction matches this specific founder's profile? The following profiles represent the clearest decision signals based on Affinitas's advisory experience.

🇦🇪 Choose the UAE if you are...

A founder or investor who is willing to physically relocate to the UAE for at least 183 days per year; who earns primarily through salary, dividends, or capital gains (all 0% personal tax); who is building international operations targeting MENA, Africa, or South/East Asia via Dubai's geographic position; who values no inheritance tax and generational wealth preservation; or who wants to consolidate global assets under a tax-efficient holding structure. The UAE is the right answer for HNWI individuals, serial entrepreneurs, family offices, and mid-to-large businesses with genuine UAE operational presence. See our free zone business setup guide and holding company setup options.

🇸🇬 Choose Singapore if you are...

A founder targeting the Asia-Pacific market who values institutional credibility with Asian and global VCs; who needs access to Singapore's deep banking ecosystem (28 of the world's top 30 banks have Singapore operations); who cannot physically relocate to the UAE but can operate from Singapore; or who is building a regulated financial services business where Singapore's MAS is the preferred regulator. Singapore is the right answer for APAC-focused businesses, fintech founders targeting regional expansion, and companies seeking VC funding from US or Asian institutional investors who prefer a familiar, credible common law jurisdiction.

🇬🇧 Choose the UK if you are...

A business that primarily serves the UK or European market and where the cost and complexity of offshore structuring exceeds the tax saving; a founder whose clients specifically require a UK entity (common in UK government contracting, financial services regulated by FCA, and professional services); a startup accessing UK-specific funding (SEIS/EIS schemes offer exceptional tax relief for investors — up to 50% income tax relief on SEIS investments); or a business that does not yet have the scale at which UAE or Singapore restructuring delivers a positive cost-benefit. The UK's Patent Box regime (10% CT on qualifying IP income) and R&D tax credits also make it compelling for deep-tech and IP-intensive businesses.

💡 Advanced Strategy: The Two-Entity Structure

Many sophisticated founders use a UAE holding company + UK or Singapore operating entity in combination. The UK or Singapore entity handles regulated local market activity, client relationships, and IP development. A UAE parent entity holds the shares, IP, and accumulates dividends from the operating company under the UAE's participation exemption — receiving them at 0% UAE personal income tax. This is not a loophole — it is standard international tax planning. But it requires professional structuring from day one. Talk to Affinitas Advisory about multi-entity structures.

Real Numbers: A $500,000 Business — UAE vs Singapore vs UK Over 5 Years

To make this concrete: consider a professional services business generating $500,000 USD profit annually, with the founder drawing the majority of profits personally. What does tax look like across five years in each jurisdiction?

| Metric | 🇦🇪 UAE (Free Zone, QFZP) | 🇸🇬 Singapore | 🇬🇧 United Kingdom |

|---|---|---|---|

| Annual Business Profit | $500,000 | $500,000 | $500,000 |

| Est. Corporate Tax | $0 (QFZP qualifying income) | ~$40,000–$55,000 (eff. ~8–11%) | ~$112,000–$125,000 (25%) |

| Post-CT profit distributed | $500,000 | ~$445,000–$460,000 | ~$375,000–$388,000 |

| Personal Income Tax on Distribution | $0 | ~$60,000–$75,000 (progressive 24%) | ~$130,000–$145,000 (45% + div tax) |

| Total Annual Tax Cost | ~$0–$15,000 (licence + compliance) | ~$100,000–$130,000 | ~$242,000–$270,000 |

| 5-Year Cumulative Tax Advantage vs UK | +$1.1M–$1.35M retained | +$550,000–$700,000 retained | — |

All figures are indicative estimates for illustrative purposes only. UAE assumes QFZP status achieved and maintained, substance requirements met. Singapore effective rate uses partial tax exemption (first SGD 10K at 4.25%, next SGD 190K at 8.5%, balance at 17%). UK assumes profits above £250K at 25% CT, additional rate income tax (45%) and 2026 dividend tax rates. Does not include professional fees, compliance costs, or personal relocation costs. Seek professional advice specific to your circumstances.

Still Deciding? Let's Think Through It Together.

Affinitas Advisory is a boutique UAE business setup and corporate tax firm based in Jumeirah Lake Towers, Dubai. We advise entrepreneurs, investors, and family offices on UAE structuring — and when UAE is not the right answer, we'll tell you that too. Our consultations are honest, not transactional.

Book Your Free 30-Minute Advisory Call →

+971 (0) 4 576 2903 · inquiries@affinitasdmcc.com · Fortune Tower, JLT, Dubai