The UAE overhauled its entire administrative tax penalty system on 14 April 2026. The good news: many fines came down significantly. The bad news — and the one that matters most for most businesses — the late payment penalty is now an uncapped 14% annual interest charge. Here is everything you need to know, from the official Cabinet Decision, explained in plain terms.

For most of its history, the UAE's tax penalty framework felt like a blunt instrument — large fixed fines for procedural errors, compounding charges that could multiply beyond the original tax liability, and limited incentive to self-correct before the FTA came knocking. Cabinet Decision No. 129 of 2025, which took effect on 14 April 2026, changes that logic significantly.

The new framework is designed around a clear principle: the government wants businesses to comply proactively and to correct errors early. Fines for administrative mistakes have come down. The window to self-correct is clearer. But the cost of simply not paying your tax on time — or waiting for the FTA to find an error rather than disclosing it yourself — is now substantially more predictable, and in many cases, more expensive over time.

The new move is aimed at simplifying tax compliance, reducing financial burden on companies and driving voluntary corrections of errors — in line with international best practices and ensuring that the UAE tax regime remains competitive and agile.— UAE Federal Tax Authority, April 2026

1. The Big One: Late Payment Is Now 14% Annual Interest

This is the change that matters most for the largest number of businesses, and it is worth understanding precisely rather than summarising.

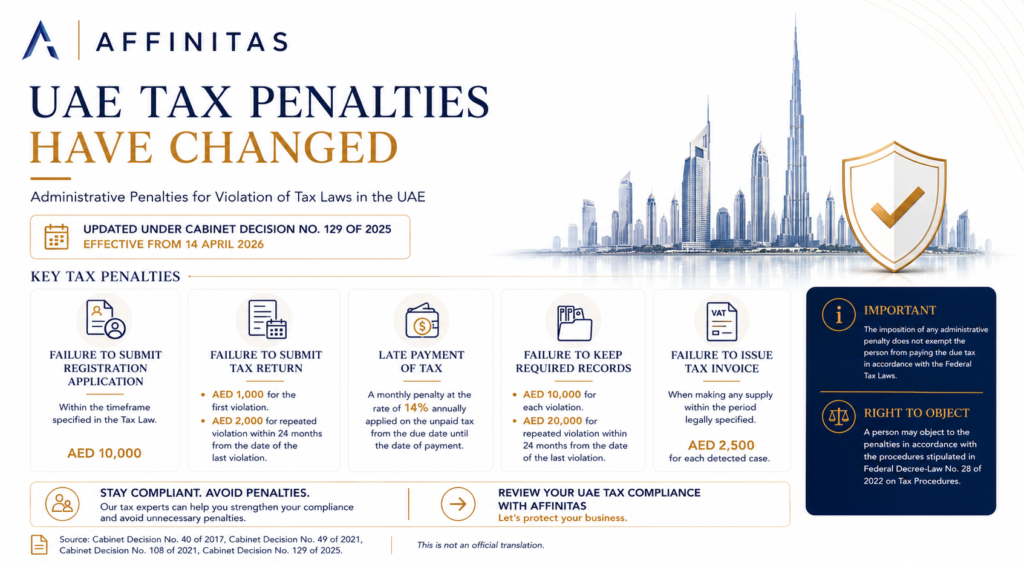

Under the old framework, late payment penalties were fixed and compounding — a structure that could produce penalties exceeding the original tax owed. Under the new framework, late payment is treated as a financial liability, not a punitive fine: 14% per annum, calculated monthly, on the unpaid tax amount, from the day after it was due. There is no maximum cap.

✕ Before April 2026

Fixed & Compounding

Multiple overlapping fixed penalties applied simultaneously. Could exceed the tax owed. Difficult to calculate in advance. Provided limited incentive to pay late rather than early.

✓ From April 2026

14% p.a. — Monthly

Simple, predictable interest charge. 14% per annum, calculated monthly on the outstanding amount. Starts the day after the due date. No maximum cap — accrues until settlement.

⚠ What 14% Actually Costs

On an unpaid VAT or Corporate Tax liability of AED 500,000, the penalty accrues at approximately AED 5,833 per month (AED 70,000 per year) until payment. Left unresolved for 12 months, the penalty alone is AED 70,000 on top of the original AED 500,000 owed. There is no cap on how long this accrues.

The 14% rate also applies in two specific scenarios with their own start dates — both worth knowing:

| Scenario | When the 14% clock starts |

|---|---|

| Standard late payment (missed deadline) | The day after the original payment due date |

| Voluntary Disclosure submitted | 20 business days after the date of VD submission |

| Tax Assessment issued by FTA | 20 business days after the date the assessment was received |

2. The Fines That Came Down: Good News for Procedural Mistakes

The administrative fines — the ones charged for procedural failures rather than unpaid tax — have been reduced materially. These changes reflect the government's view that most businesses make administrative errors through oversight, not intent, and that the penalty should fit the offence.

| Violation | Old Penalty | New Penalty (from April 2026) | Direction |

|---|---|---|---|

| Not submitting records in Arabic when FTA requests | AED 20,000 | AED 5,000 | ↓ 75% lower |

| Not updating tax record information | AED 5,000 (first) / AED 10,000 (repeat) | AED 1,000 (first) / AED 5,000 (repeat within 24 months) | ↓ Significantly lower |

| Legal representative not notifying FTA of appointment | AED 10,000 | AED 1,000 | ↓ 90% lower |

| Legal rep fails to file tax return on time | AED 10,000 | AED 1,000 (first) / AED 2,000 (repeat within 24 months) | ↓ Lower |

| Registrant fails to file Tax Return on time | Varied | AED 1,000 (first) / AED 2,000 (repeat within 24 months) | ↓ Simplified and lower |

| Record keeping failure | AED 10,000 (first) / AED 50,000 (repeat) | AED 10,000 (first) / AED 20,000 (repeat within 24 months) | ↓ Repeat penalty reduced |

| Failure to register for tax (VAT) | AED 20,000 | AED 10,000 | ↓ 50% lower |

| Late CT Registration | AED 10,000 | AED 10,000 | — Unchanged |

📌 Important: CT Registration Penalty Did Not Change

While many fines fell, the AED 10,000 penalty for late Corporate Tax registration was not reduced. Every UAE business — including Free Zone entities — must register for CT regardless of profit level. If you have not yet registered, Affinitas can complete your registration within 48 hours.

3. Voluntary Disclosure: The Maths of Coming Clean Early

The new framework puts significant emphasis on Voluntary Disclosure — the mechanism by which businesses self-report errors in their tax filings before the FTA discovers them. The penalty structure for VD is now much clearer, and it creates a strong financial incentive to act before the FTA sends an audit notification.

| Situation | Penalty on Tax Difference | Verdict |

|---|---|---|

| VD submitted before any FTA audit notification | 1% per month on the tax difference — from original due date to VD submission date | ✓ Best outcome available |

| VD submitted after FTA audit notification | 15% fixed penalty on tax difference + 1% per month from original due date to VD date | ✕ Much more expensive |

| No VD submitted — FTA issues Tax Assessment | 15% fixed penalty + 1% per month from original due date to assessment date + 14% annual interest on unpaid tax | ✕ Most expensive outcome |

The practical implication: if your business has historical tax errors — incorrect VAT returns, understated CT liability, missing documentation — the time to address them is before the FTA contacts you. The 1% monthly charge on a VD submitted now is substantially less painful than the 15% fixed penalty plus interest that applies the moment an audit notification arrives.

4. VAT-Specific Penalties: What Changed

Table 3 of the Cabinet Decision covers VAT violations directly. Several penalties that previously caught businesses off-guard have been clarified.

| VAT Violation | Penalty (from April 2026) |

|---|---|

| Not displaying prices inclusive of VAT | AED 5,000 |

| Not notifying FTA of applying tax on margin scheme | AED 2,500 |

| Not issuing a Tax Invoice within the legally required period | AED 2,500 per detected case |

| Not issuing a Tax Credit Note within the required period | AED 2,500 per detected case |

| Not complying with e-invoicing conditions for Tax Invoice or Credit Note | AED 2,500 per detected case |

| Goods in Designated Zone — non-compliance | Higher of AED 50,000 or 50% of the applicable tax |

The AED 2,500 per-case penalty for missing or incorrect invoices is worth particular attention as the UAE's mandatory e-invoicing rollout approaches. From January 2027, all covered B2B and B2G invoices must be transmitted through an Accredited Service Provider. Non-compliant invoices will attract the AED 2,500 penalty per case — and in businesses with high invoice volumes, those cases add up rapidly.

5. One Framework, Three Tax Regimes

One of the most practically significant changes in the new regime is structural rather than numerical. Cabinet Decision No. 129 of 2025 harmonises the penalty framework across all three UAE tax regimes — VAT, Excise Tax, and Corporate Tax — using the same definitions, timelines, and calculation methods.

✓ What Harmonisation Means for You

If your business operates across multiple tax regimes — VAT-registered and CT-registered, for example — you no longer need to track different penalty calculation methodologies for each. The 14% late payment rate, the 1% VD monthly charge, and the 15% post-audit fixed penalty all apply consistently. Compliance management becomes simpler — and the consequences of getting it wrong are the same regardless of which tax was underpaid.

Frequently Asked Questions

Is the 14% interest rate applied daily or monthly?

The legislation states 14% per annum, for each month or part thereof, imposed on the same date monthly. The Cabinet Decision refers to a monthly calculation at the annualised rate of 14%, meaning approximately 1.17% per month. It applies on any part of a month — so a payment that is one day late still attracts a full month's charge.

Does the new penalty framework apply retroactively?

No. Cabinet Decision No. 129 of 2025 took effect on 14 April 2026. Penalties for violations that occurred before that date are assessed under the prior framework. For businesses with historical errors that they have not yet disclosed, the new VD penalty structure (1% per month) applies to disclosures made on or after 14 April 2026 — which in most cases is more favourable than the old compounding system for the period from 14 April 2026 forward.

We missed a VAT return deadline. What is our penalty?

Two charges apply. First, a fixed AED 1,000 for the late submission of the return itself (AED 2,000 if this has happened before within 24 months). Second, if any tax was underpaid as a result, the 14% annual interest charge applies on the unpaid amount from the day after the original due date. Contact Affinitas to assess the total exposure and determine whether a Voluntary Disclosure is appropriate before the FTA initiates contact.

I have an error in a past VAT return. Should I file a Voluntary Disclosure?

Almost certainly yes, and before the FTA contacts you. The penalty for a VD submitted proactively is 1% per month on the tax difference — predictable, calculable, and significantly lower than the 15% fixed penalty plus 1% monthly that applies if you submit after receiving an audit notification. Affinitas reviews your specific situation and manages the VD process on your behalf.

Related from Affinitas

- Corporate Tax Registration — Avoid the AED 10,000 Late Registration Penalty

- UAE Transfer Pricing 2026 — The 14% Interest Rate Applies to TP Adjustments Too

- Accounting & Tax Compliance Services — Ongoing FTA compliance management

- Tax Advisory — Voluntary Disclosure and FTA audit support

Not Sure What These Changes Mean for Your Business?

Affinitas provides tax compliance advisory, Voluntary Disclosure support, and FTA audit defence. One call identifies your exposure and the most cost-effective path to resolution.

+971 (0) 4 576 2903 | inquiries@affinitasdmcc.com