The UAE Corporate Tax landscape has undergone one of its most significant developments since the regime was introduced in June 2023.

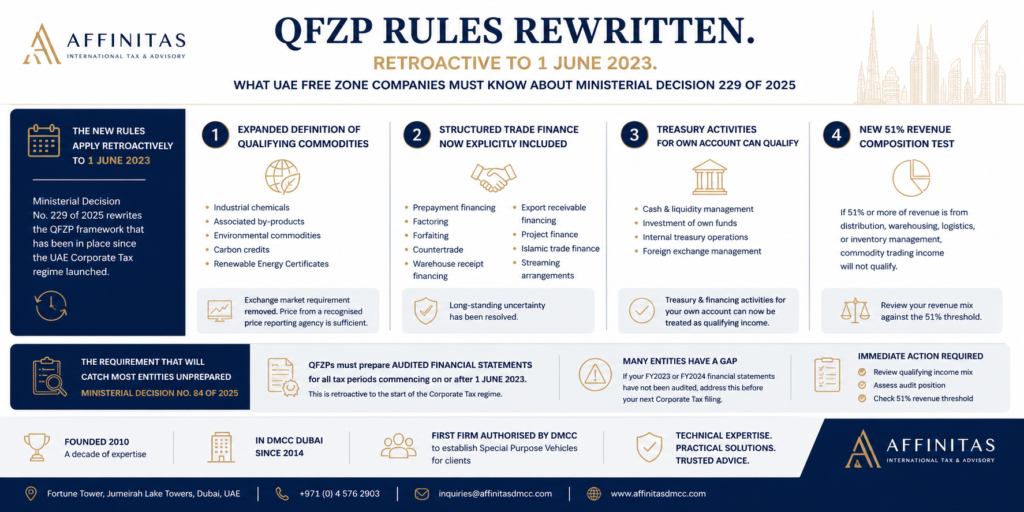

With the issuance of Ministerial Decision No. 229 of 2025, the UAE Ministry of Finance has effectively rewritten the framework governing Qualifying Free Zone Persons (QFZPs). More importantly, the changes apply retroactively from 1 June 2023, meaning businesses must reassess positions they may have relied upon for the last two years.

For many Free Zone companies, this is not merely a technical amendment. It could directly affect eligibility for the highly valuable 0% Corporate Tax rate.

Companies that previously concluded they qualified under the original framework may now find that their position requires reassessment. Equally, some businesses that were uncertain about qualification may now discover new opportunities under the expanded rules.

The implications are significant, particularly for commodity traders, holding companies, treasury centers, logistics businesses, SPVs, and international structures operating from UAE Free Zones.

Why Ministerial Decision 229 of 2025 Matters

When the UAE introduced Corporate Tax, Free Zone entities were offered access to a 0% Corporate Tax rate provided they met the requirements of being a Qualifying Free Zone Person (QFZP).

The original framework was established under Ministerial Decision No. 265 of 2023.

However, Ministerial Decision 229 of 2025 effectively replaces substantial portions of that framework and introduces new interpretations, clarifications, and qualification criteria that apply retrospectively.

The practical consequence is straightforward:

"A QFZP assessment performed under the original framework may no longer be sufficient after August 2025."

Businesses must review historical positions covering every tax period since June 2023.

Understanding the Importance of QFZP Status

Maintaining QFZP status remains one of the most valuable tax incentives available in the UAE.

A qualifying entity may benefit from:

| Benefit | Impact |

|---|---|

| 0% Corporate Tax Rate | On qualifying income |

| Enhanced International Competitiveness | Reduced effective tax burden |

| Greater Investment Attraction | Tax-efficient structuring |

| Regional Headquarters Benefits | Centralized operations in UAE |

| Treasury and Holding Functions | Potential tax optimization opportunities |

However, failure to comply with the QFZP requirements can result in losing eligibility and becoming subject to the standard Corporate Tax regime.

Key Change #1: Expanded Definition of Qualifying Commodities

One of the most notable changes introduced by Ministerial Decision 229 of 2025 is the expansion of what constitutes a qualifying commodity.

Previously, qualification was largely tied to trading through recognized commodity exchanges.

The revised framework broadens the scope considerably.

Newly Recognized Categories Include:

- Industrial chemicals

- Associated by-products

- Environmental commodities

- Carbon credits

- Renewable Energy Certificates (RECs)

In addition, the requirement for transactions to occur through a recognized exchange market has been removed.

Instead, pricing established by a recognized price reporting agency may now satisfy qualification requirements.

Why This Matters

This change opens the door for numerous businesses operating in:

- Energy trading

- Sustainability markets

- Carbon credit projects

- Environmental finance

- Industrial commodity distribution

to potentially qualify where uncertainty previously existed.

Key Change #2: Structured Trade Finance Is Now Explicitly Included

Since the launch of UAE Corporate Tax, advisers and businesses have debated whether various structured financing arrangements could be considered qualifying activities.

Ministerial Decision 229 of 2025 finally provides clarity.

The following transactions are now expressly recognized within qualifying commodity trading activities:

| Structured Finance Activity | Status Under MD 229/2025 |

|---|---|

| Prepayment Financing | Qualifying |

| Factoring | Qualifying |

| Forfaiting | Qualifying |

| Countertrade Arrangements | Qualifying |

| Warehouse Receipt Financing | Qualifying |

| Export Receivable Financing | Qualifying |

| Project Finance Structures | Qualifying |

| Islamic Trade Finance | Qualifying |

| Streaming Arrangements | Qualifying |

This clarification removes a major area of uncertainty that existed throughout the first two years of the Corporate Tax regime.

Key Change #3: Treasury Activities for Own Account Can Now Qualify

Another significant development concerns treasury operations.

Historically, many groups questioned whether a Free Zone entity managing its own cash reserves, investments, and liquidity could generate qualifying income.

Ministerial Decision 229 of 2025 now provides confirmation that treasury and financing activities conducted for the entity's own account may fall within qualifying activities.

Examples may include:

- Cash management

- Liquidity management

- Internal treasury operations

- Investment of surplus funds

- Foreign exchange management

For holding structures and investment vehicles, this clarification could materially affect tax planning strategies.

Key Change #4: The New 51% Revenue Composition Test

Perhaps the most overlooked aspect of the new framework is the introduction of a revenue composition threshold.

Under the revised rules:

If 51% or more of a QFZP's revenue is derived from distribution, warehousing, logistics, or inventory management functions, commodity trading income may no longer qualify.

This represents a substantial compliance consideration.

Businesses Potentially Impacted

- Trading companies with warehouse operations

- Regional distribution hubs

- Logistics-focused commodity businesses

- Import-export companies

- Integrated supply chain businesses

Revenue Mix Illustration

| Revenue Source | Percentage |

|---|---|

| Commodity Trading | 45% |

| Warehousing Services | 25% |

| Distribution Activities | 20% |

| Inventory Management | 10% |

Total logistics-related activities = 55%

Result: Potential QFZP qualification risk.

This analysis now becomes a critical component of every QFZP review.

The Compliance Requirement That Could Catch Many Companies Off Guard

While most businesses are focusing on qualifying activities, another development may present an even greater challenge.

Ministerial Decision No. 84 of 2025 introduces a requirement for QFZPs to maintain audited financial statements for tax periods beginning on or after 1 June 2023.

This requirement applies retroactively.

Why This Is Significant

Many Free Zone entities have historically operated with:

- Management accounts

- Internal bookkeeping records

- Unaudited financial statements

This has been particularly common among:

- Holding companies

- SPVs

- Family office structures

- Investment entities

- Asset holding vehicles

Under the revised framework, these businesses may now face a compliance gap.

QFZP Audit Requirements: What Businesses Need to Check

Every Free Zone company should immediately assess:

Financial Year 2023

- Were audited financial statements prepared?

- Were audits completed by a qualified auditor?

Financial Year 2024

- Have audited statements been finalized?

- Is audit documentation available?

Future Periods

- Is the company maintaining records sufficient for audit requirements?

- Are internal controls aligned with Corporate Tax expectations?

Failure to address these questions before Corporate Tax filings could create unnecessary exposure.

What UAE Free Zone Companies Should Do Now

1. Reassess QFZP Qualification

Review all qualifying activities under the revised framework.

The analysis should cover every Corporate Tax period beginning from June 2023.

2. Review Historical Tax Positions

Many businesses relied on interpretations developed before the publication of Ministerial Decision 229 of 2025.

Those positions should be revisited to ensure continued compliance.

3. Verify Audit Readiness

Confirm whether FY2023 and FY2024 audited financial statements are available and compliant with current requirements.

4. Examine Revenue Composition

The new 51% threshold requires a detailed breakdown of income sources.

Businesses with mixed operational models should pay particular attention.

5. Seek Specialist Corporate Tax Advice

The interaction between:

- Qualifying activities

- Revenue thresholds

- Audit requirements

- Transfer pricing

- Related party transactions

- Free Zone regulations

creates a highly technical compliance environment.

Professional review is increasingly essential.

Expert Perspective

As the UAE Corporate Tax framework matures, regulators are moving from broad principles toward increasingly detailed qualification tests.

The retroactive application of Ministerial Decision 229 of 2025 demonstrates the importance of ongoing tax governance rather than relying solely on assessments performed when Corporate Tax was first introduced.

"The most significant risk is not necessarily non-compliance today—it is assuming that a conclusion reached in 2023 remains valid in 2025 without reassessment."

For many Free Zone businesses, the opportunity remains substantial. However, maintaining access to the 0% Corporate Tax rate now requires a higher level of documentation, audit readiness, and technical review.

How Affinitas Can Help

Founded in 2010 and operating in Dubai since 2014, Affinitas has extensive experience supporting international investors, holding structures, SPVs, commodity trading companies, and Free Zone entities navigating UAE tax and compliance requirements.

Our specialists can assist with:

- QFZP eligibility reviews

- Corporate Tax registration

- Corporate Tax filing

- Transfer Pricing assessments

- SPV structuring

- Holding company structures

- Audit coordination

- Tax residency planning

- International tax advisory

Related Services

- Corporate Tax Registration in Dubai and Abu Dhabi

- Holding vs SPV in the UAE: Which Structure Is Right for You?

- Affinitas Contact Page

Contact Affinitas

Affinitas

Fortune Tower, Jumeirah Lake Towers, Dubai, UAE

Phone: +971 (0) 4 576 2903

Email: inquiries@affinitasdmcc.com

Sources

- Ministerial Decision No. 229 of 2025

- Ministerial Decision No. 84 of 2025

- UAE Ministry of Finance

- Federal Tax Authority UAE

Disclaimer: This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Businesses should seek professional advice based on their specific circumstances.