The introduction of UAE Corporate Tax has pushed Transfer Pricing (TP) to the forefront of compliance for all UAE businesses — from small family-owned companies to multinational groups with complex structures.

The UAE is now fully aligned with OECD Base Erosion and Profit Shifting (BEPS) standards, meaning companies must justify all related-party transactions using the Arm’s Length Principle, supported by proper documentation.

Many UAE companies mistakenly assume transfer pricing is “only for large corporations.”

This is no longer true.

In 2025, SMEs and Free Zone companies fall under TP rules as well — and non-compliance carries serious penalties and audit risks.

1. What Is Transfer Pricing?

Transfer Pricing governs how prices are set for transactions between related parties, including:

- Parent → subsidiary

- Subsidiary → subsidiary

- Shareholder’s foreign company → UAE company

- UAE Free Zone → UAE Mainland

- Owner-managed companies

- Family-owned groups

- SPVs and holding companies

Examples of related-party transactions:

- Management fees

- Royalty or IP charges

- Service fees

- Intercompany loans

- Cost recharges

- Sale of goods between group companies

- Director compensation (in many cases treated as related-party transactions)

These transactions must be priced as if the parties were independent (Arm’s Length Principle).

Source:

OECD Transfer Pricing Guidelines

2. Why Transfer Pricing Matters in the UAE

The UAE Corporate Tax Law requires companies to:

- Apply the Arm’s Length Principle

- Maintain TP documentation

- File a Transfer Pricing Disclosure Form

- Submit Master File and Local File (in applicable cases)

- Justify all related-party transactions

The Federal Tax Authority (FTA) is placing significant focus on TP in 2025 because:

- Many companies are owned by families or groups

- Free Zone & Mainland companies frequently transact with each other

- Multinationals shift income through IP or service fees

- SMEs use intercompany loans without justification

Failure to comply can lead to:

- Adjusted profit calculations

- Loss of Qualifying Free Zone (0%) status

- Backdated taxes

- Penalties

- Full TP audit

3. Who Must Comply With Transfer Pricing in the UAE?

Every UAE business with any related-party transactions.

This includes:

SMEs

Even a small Free Zone company paying:

- salary to owner

- fee to shareholder’s company abroad

- intercompany service fee

…must comply.

Multinationals

Required to prepare:

- Master File

- Local File

- CbCR (Country-by-Country Reporting) where applicable

Free Zone Companies

Especially relevant for those seeking the 0% Qualifying Free Zone rate:

- Any related-party mispricing can disqualify the company from 0%.

Holding Companies & SPVs

Even passive structures must comply with TP rules if they:

- hold assets

- pay/receive shareholder loans

- allocate costs

4. Key Transfer Pricing Requirements in the UAE

4.1. Arm’s Length Principle

You must prove that your related-party transactions are priced the same as they would be between independent companies.

Five accepted TP methods (OECD):

- Comparable Uncontrolled Price (CUP)

- Resale Price Method

- Cost-Plus Method

- Transactional Net Margin Method (TNMM)

- Profit Split Method

4.2. Transfer Pricing Disclosure Form

This must be filed together with the Corporate Tax Return.

Disclosure is mandatory for:

- All companies with related-party transactions

The FTA uses this form to identify which businesses are likely to be audited.

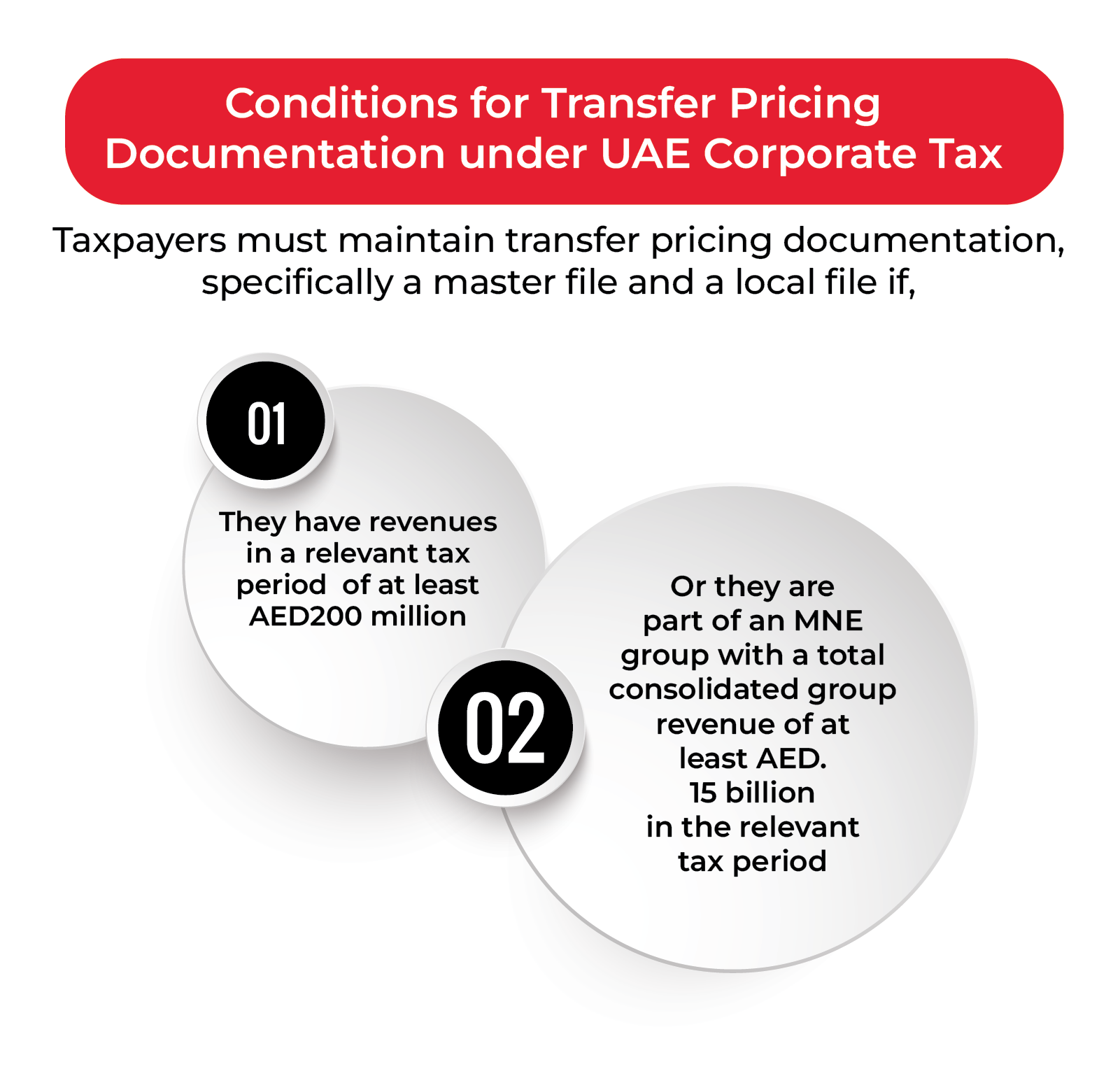

4.3. Master File

Required for multinational or large entities belonging to a group that meets FTA thresholds.

Contains:

- Group structure

- Global business overview

- IP ownership

- Transfer pricing policies

4.4. Local File

Required for entities exceeding revenue or asset thresholds.

Contains:

- Detailed descriptions of related-party transactions

- Benchmarking

- Economic analysis

- Functional analysis (FAR)

4.5. Documentation Must Be Maintained Annually

Even if not requested, companies must keep:

- Agreements

- Benchmark studies

- Financial segregation

- Pricing analysis

- Intra-group policies

5. Common Transfer Pricing Risks for UAE Businesses

Risk 1: Owner salary treated as related-party income

Many SMEs structure compensation incorrectly.

Risk 2: Free Zone companies losing 0% because of TP

Non-arm’s-length pricing → disqualified from Qualifying Income.

Risk 3: Intercompany loans with no interest or benchmark

FTA considers interest-free related loans a TP risk.

Risk 4: Payments to shareholder’s foreign company

Requires benchmarking and agreements.

Risk 5: Mispricing for Mainland ⇆ Free Zone transactions

Especially dangerous for businesses trying to qualify for 0%.

Risk 6: Cost-sharing agreements without documentation

High audit trigger.

Risk 7: Multinationals shifting profit through service fees

FTA expects:

- substance

- economic benefit proof

- benchmarking

6. Case Study: Free Zone Company Losing 0% Rate

A DMCC company provides “consulting services” to its Mainland sister company.

It charged AED 10,000/month based on owner estimates.

FTA assessment:

- No benchmarking

- No written service agreement

- No proof of substance

- Below-market pricing

- Mainland company over-deducted expenses

Result:

DMCC company loses access to 0% Qualifying Income, pays 9%.

How Businesses Can Ensure Transfer Pricing Compliance

✔ Prepare a TP policy

✔ Draft intercompany agreements

✔ Benchmark service fees, loans, royalties

✔ Document management fees

✔ Use OECD-approved methods

✔ Maintain evidence of substance

✔ Separate Free Zone & Mainland income clearly

✔ Prepare for FTA inquiries or audits

Most importantly:

Don’t wait until filing season.

TP mistakes are much harder to fix retroactively.

How Affinitas DMCC Helps With Transfer Pricing

Affinitas provides end-to-end TP solutions:

✔ Transfer Pricing Policy Creation

✔ Transfer Pricing Documentation (Local File & Master File)

✔ Transfer Pricing Disclosure Form preparation

✔ Intercompany Agreements (loans, services, royalties)

✔ Benchmarking Studies (OECD-compliant)

✔ Free Zone Qualifying Income structuring

✔ Audit support & representation

✔ Group structuring for tax optimisation

We work with:

- SMEs

- Free Zone companies

- Multinationals

- Holding/SPV structures

- E-commerce groups

- Family-owned businesses

Transfer Pricing Is Now a Critical Compliance Requirement

Transfer Pricing is not a technical detail — it is one of the most important compliance obligations under the UAE Corporate Tax Law.

Companies that implement proper TP policies will:

- Protect 0% Free Zone status

- Avoid penalties

- Pass FTA audits

- Reduce tax risks

- Strengthen group governance

Those who ignore TP rules face:

- Backdated taxes

- Loss of tax benefits

- Significant penalties

- Audit investigations

2025 is the year to build strong, compliant transfer pricing systems — especially before filing your corporate tax return.

Get Expert Transfer Pricing Support Today

Launch Your Business In Dubai and the Entire UAE

Get Your Free Consultation with Our Business Consultants!

📞 +971 (0) 4 576 2903

📧 in*******@af***********.com

📍 Fortune Tower, Jumeirah Lake Towers — Dubai

🔗 https://affinitasdmcc.com/contact/