What Changed in January 2026 — and Why It Is Different This Time

The UAE has participated in international tax transparency initiatives for over a decade. It joined the OECD Global Forum on Transparency and Exchange of Information for Tax Purposes and signed various bilateral exchange agreements. What the UAE lacked, until now, was domestic operational machinery — a codified, enforceable, penalty-backed domestic law that compelled the UAE Federal Tax Authority (FTA) to act on foreign information requests within defined timeframes.

Cabinet Decision No. 209 of 2025 fills that gap. It is not a new political stance. It is the final structural piece that converts the UAE's international commitments into a working domestic system. The previous framework, established in 2012, was narrow in scope and not fully aligned with the OECD's Exchange of Information on Request (EOIR) standard. The new framework covers every legal person and arrangement registered in the UAE — including free zone entities, foundations, partnerships, and SPVs.

The question is not whether your UAE structure will eventually be visible to relevant tax authorities. It is whether what they see is the result of deliberate, well-documented planning — or something that accumulated over years without review.— Affinitas Advisory Team, Jumeirah Lake Towers, Dubai

Good intentions have been replaced by operational machinery. That is a precise and important distinction.

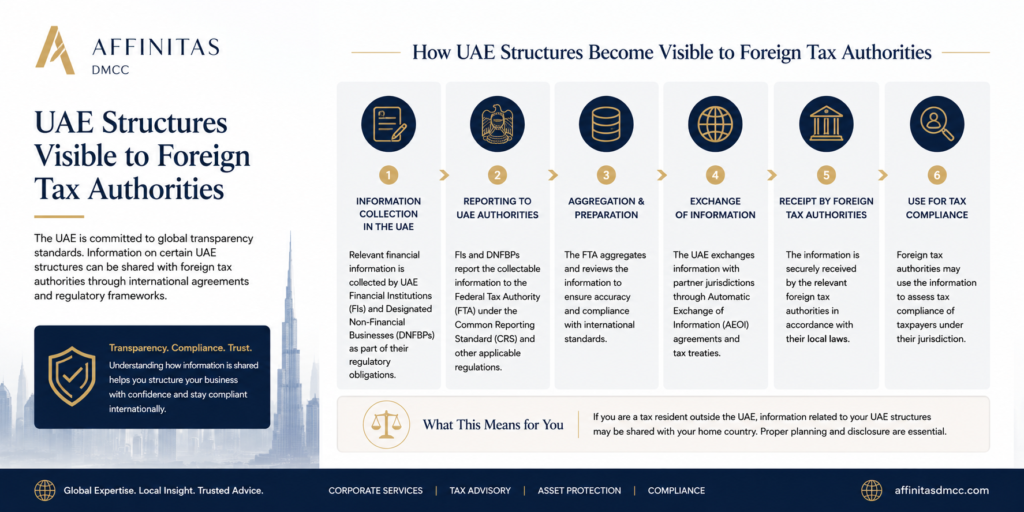

How EOIR Actually Works: What It Is and What It Is Not

There is widespread confusion about what Exchange of Information on Request means in practice. It is not automatic reporting — a foreign tax authority does not receive a live feed of your UAE income, account balances, or ownership structure. It operates differently, and understanding the mechanics matters.

| Feature | EOIR (Exchange on Request) | AEOI / CRS (Automatic Exchange) |

|---|---|---|

| How it is triggered | A foreign tax authority submits a specific, legally grounded request | Automatic — data transmitted annually without any request |

| What is required | A treaty or exchange agreement between the two jurisdictions | Participation in CRS / FATCA framework |

| Scope | Targeted — specific taxpayer or transaction | Broad — covers all qualifying financial accounts |

| FTA obligation (post-Dec 2025) | Legally required to collect and deliver within defined timeframes | Separate obligations under UAE CRS law |

| Penalty for non-compliance (UAE entity) | Attached to failure to maintain required records | Separate CRS penalty regime |

| Who is exposed | All UAE legal persons, including Free Zone entities | Financial institutions and their account holders |

When a foreign tax authority — the Russian Federal Tax Service (FNS Russia), HMRC, Germany's Bundeszentralamt für Steuern, or any other counterpart with whom the UAE has an exchange agreement — submits a valid EOIR request, the FTA is now required to act. The UAE cannot simply decline to engage or delay indefinitely, as was possible under the pre-2026 framework.

The Russia Dimension: Why January 2026 Is Particularly Significant

For Russian nationals and businesses with UAE structures, two developments converged simultaneously on 1 January 2026, creating a compound shift in exposure.

First: the Russia-UAE double taxation treaty entered into force. The treaty contains a standard information exchange article — providing the legal basis for EOIR requests between the two jurisdictions. Second: the UAE was removed from Russia's list of offshore jurisdictions. This is counterintuitive to many clients. Removal from the offshore list does not mean the UAE is now treated with less scrutiny by Russian tax authorities. It means the opposite: UAE income and structures are no longer categorically flagged as offshore and therefore suspicious — they are now treated as legitimate foreign income subject to normal Russian tax rules, including controlled foreign company (CFC) reporting, dividend taxation, and transfer pricing provisions.

⚠ Direct Implication for Russian Nationals

The Russian Federal Tax Service now has both the legal treaty basis and an operational domestic UAE mechanism — EOIR under Cabinet Decision No. 209 — to formally request information about your UAE structure. The combination that existed six months ago no longer exists. Read Affinitas' detailed analysis of the Russia-UAE offshore list change →

For European and British clients, the position is not new in principle. HMRC, Germany's BZSt, Italy's Agenzia delle Entrate, and the Dutch Belastingdienst have used EOIR mechanisms with other jurisdictions for years. The difference is operational: requests to the UAE can now be actioned through a clear, penalty-backed domestic framework rather than a pre-2026 process characterised by administrative friction and uncertain timelines.

Three Areas of Immediate Exposure

The EOIR framework does not create new tax liabilities. It creates a new collection and transmission mechanism for information that may reveal existing ones. Three areas warrant immediate review for most UAE-based structures.

1. Beneficial Ownership Records

Beneficial ownership information is one of the primary categories of information a foreign tax authority will request. The EOIR framework makes current, accurate UBO records a live compliance requirement — not an administrative formality. UAE entities are legally required to maintain accurate, up-to-date records. If those records are stale, reflect a structure that has evolved since incorporation, or contain nominee arrangements that were not properly documented, that gap is the first thing a requesting authority will probe.

2. Historic ESR Positions (FY2019–2022)

This is where many clients are surprised. The UAE Ministry of Finance introduced Economic Substance Regulations (ESR) in 2019, requiring UAE entities engaged in relevant activities to demonstrate genuine economic substance — real people, real decisions, real costs — in the UAE. Under legislation effective January 2026, the FTA has a 15-year audit window for ESR compliance. Entities that failed to register, file, or meet substance requirements in FY2019 through FY2022 are not in the clear simply because those years have passed.

| ESR Compliance Period | Auditable Under 15-Year Window? | EOIR Risk if Non-Compliant | Recommended Action |

|---|---|---|---|

| FY2019 | ✓ Yes — until 2034 | High | Historical ESR exposure assessment |

| FY2020 | ✓ Yes — until 2035 | High | Historical ESR exposure assessment |

| FY2021 | ✓ Yes — until 2036 | High | Historical ESR exposure assessment |

| FY2022 | ✓ Yes — until 2037 | Medium–High | Historical ESR exposure assessment |

| FY2023 onwards | ✓ Yes — rolling window | Depends on compliance status | Ongoing compliance management |

An ESR finding by the FTA can independently trigger information exchange with the home-country authority. EOIR and ESR now operate in parallel — a failure in one feeds the other.

3. Intercompany Pricing and Transfer Pricing Documentation

If a foreign tax authority requests information about payments flowing between a UAE entity and a related party in their jurisdiction, the FTA will provide what it holds. A Transfer Pricing Disclosure Form on file is not a defence in itself. The relevant question is whether the methodology behind the intercompany prices withstands scrutiny in both jurisdictions simultaneously — under UAE Transfer Pricing rules and under the home-country's arm's-length standard.

Transfer pricing is the FTA's primary audit tool in 2026. A disclosure form filed without a supporting benchmarking study and documented methodology is compliance theatre, not compliance.— Affinitas Advisory Team

Who Is Most Exposed: A Practical Risk Matrix

| Client Profile | EOIR Exposure | Primary Risk Factor | Priority Action |

|---|---|---|---|

| Russian national with UAE Free Zone entity established pre-2023 | High | New Russia-UAE DTA + EOIR framework operational simultaneously | UBO review + ESR assessment + TP review |

| UK/EU resident using UAE holding company for offshore income | High | HMRC/BZSt/Agenzia delle Entrate have active EOIR programmes | Cross-border tax consistency review |

| UAE Free Zone entity with intercompany transactions | Medium–High | TP Disclosure Form without supporting documentation | Transfer pricing documentation |

| UAE entity that did not file ESR (FY2019–2022) | High | 15-year FTA audit window + EOIR parallel risk | Historical ESR exposure assessment |

| Foundation or trust structure with UAE-based assets | Medium | EOIR covers foundations and arrangements explicitly | Governance review + UBO records update |

| UAE entity with current, accurate records and documented TP methodology | Low | Nothing to hide is the best position — but must be provable | Periodic compliance review to maintain position |

The QFZP Connection: Free Zone Is No Longer a Safe Harbour

A separate but related development compounds the EOIR risk for Free Zone entities. The Qualifying Free Zone Person (QFZP) rules were rewritten with retroactive effect in 2026. Entities that assumed Free Zone status automatically conferred 0% corporate tax protection may now find that their position was not compliant — either in the current period or historically.

A QFZP disqualification finding does two things simultaneously: it creates a UAE corporate tax liability, and it creates information that a foreign tax authority may request through EOIR. The two risks feed each other.

Related: QFZP Rules Rewritten with Retroactive Effect

Every UAE Free Zone entity should reassess its corporate tax position in light of the 2026 QFZP amendments. Affinitas has published a detailed guide to what changed and who is affected. Read the full analysis →

How to Respond: A Structured Approach to EOIR Readiness

The correct response to this framework is not alarm. It is structure. The entities that are well-positioned under EOIR are not the ones with complex arrangements — they are the ones whose arrangements are accurate, documented, and defensible. The timeline below represents the logical sequence for any review.

1 EOIR Readiness Review

Map all UAE entities and arrangements against the EOIR framework. Identify what information the FTA holds about each structure and whether it is current and accurate.

2 UBO and Beneficial Ownership Compliance Review

Verify that all UAE entity beneficial ownership records are current, complete, and match the actual ownership structure. Update where the entity has changed since incorporation.

3 Historical ESR Exposure Assessment (FY2019–2022)

Determine whether the entity was required to register and file under ESR in each year. Assess the risk position and identify any remediation steps available.

4 Transfer Pricing and Intercompany Transaction Review

Review all related-party transactions. Confirm that pricing is supported by a documented arm's-length methodology defensible under both UAE and home-country rules.

5 Foundation, Holding Company and SPV Governance Review

Verify that governance structures, board minutes, and operational substance records support the legal arrangements in place.

6 Cross-Border Tax Consistency Review

Confirm that UAE filings and home-country filings are consistent. Discrepancies between what the UAE holds and what a taxpayer has declared in their home jurisdiction are precisely what EOIR requests are designed to surface.

How Affinitas Supports EOIR Readiness

Affinitas has operated from DMCC Dubai since 2014 and was the first firm authorised by DMCC to establish Special Purpose Vehicles for clients when that product launched. Our team includes advisers with ADIT, CTA, and Big 4 credentials, and our transfer pricing practice operates at a depth most UAE advisory firms cannot match.

The services below are specifically designed to ensure that the information available to UAE authorities — and therefore to foreign tax authorities through EOIR — is accurate, complete, and defensible before any request is received.

EOIR Readiness Reviews

Full assessment of UAE structure visibility under the new framework and identification of records gaps.

UBO & Beneficial Ownership Reviews

Verification and update of beneficial ownership records across all UAE entities.

Historical ESR Exposure Assessments

FY2019–2022 review of ESR filing positions, risk quantification, and remediation options.

Transfer Pricing Documentation

End-to-end TP documentation, benchmarking studies, and audit defence for UAE and cross-border positions.

Foundation, Holding & SPV Governance Reviews

Governance documentation, board minute structuring, and substance verification.

Cross-Border Tax Consistency Reviews

Alignment of UAE filings with home-country declarations — the most direct EOIR risk mitigation available.

FTA Information Request Support

Representation and advisory support if an FTA information request has already been received.

Corporate Tax Registration & Compliance

For entities not yet registered — registration completed within 48 hours on average.

Frequently Asked Questions

What is Cabinet Decision No. 209 of 2025?

Cabinet Decision No. 209 of 2025 is the UAE's new domestic legal framework for responding to Exchange of Information on Request (EOIR) submissions from foreign tax authorities. It replaces the 2012 framework and aligns the UAE with the OECD's EOIR standard, covering all legal persons and arrangements registered in the UAE, including free zone entities, foundations, and partnerships.

Does the UAE automatically share my financial information with foreign governments?

No. EOIR is triggered by a specific request from a foreign tax authority, not by automatic transmission. The UAE also participates in the OECD's Common Reporting Standard (CRS) for automatic exchange of financial account information — a separate and parallel system. Cabinet Decision No. 209 governs the EOIR channel specifically.

Are UAE Free Zone entities covered?

Yes. Cabinet Decision No. 209 of 2025 explicitly covers all legal persons and arrangements registered in the UAE, with no carve-out for Free Zone entities. This includes DMCC, DIFC, JAFZA, ADGM, and all other Free Zone registered entities.

What is the ESR audit window, and why does it start in 2019?

The UAE introduced Economic Substance Regulations in 2019. Under legislation effective January 2026, the FTA has a 15-year audit window for ESR compliance — meaning FY2019 positions remain auditable until 2034. Entities that failed to register or file in any year from FY2019 onwards are exposed.

What should I do if I have already received a communication from the FTA?

Contact an adviser immediately. Do not respond to FTA information requests without professional support. Affinitas provides direct advisory assistance for FTA enquiries — contact the team here.

Related Affinitas Resources

- The UAE Just Left Russia's Offshore Blacklist — What It Means for Your Structure

- QFZP Rules Rewritten with Retroactive Effect — Full Analysis

- Transfer Pricing in the UAE — Affinitas Guide

- Corporate Tax Registration in Dubai and Abu Dhabi

- Holding Companies vs SPVs in the UAE

- Compliance Management Services — Affinitas

- DMCC SPV Setup — Affinitas is Dubai's First Registered DMCC SPV Agent

Sources & External References

- UAE Federal Tax Authority — tax.gov.ae

- OECD Global Forum on Transparency and Exchange of Information for Tax Purposes

- OECD — Automatic Exchange of Information (CRS / AEOI)

- UAE Federal Decree-Law No. 47 of 2022 — Corporate Tax

- UAE Ministry of Finance — Economic Substance Regulations

- Federal Tax Service of Russia (FNS) — nalog.gov.ru

- HM Revenue & Customs (HMRC) — gov.uk

- Bundeszentralamt für Steuern (Germany) — bzst.de

- OECD — Pillar Two Global Minimum Tax

- DMCC — Dubai Multi Commodities Centre

© 2026 Affinitas. Fortune Tower, Cluster C, Jumeirah Lake Towers, Dubai, UAE. This article is for informational purposes only and does not constitute legal, tax, or financial advice. Always seek professional advice specific to your circumstances.

Is Your UAE Structure Defensible?

An Affinitas adviser will review your position and identify exactly where exposure exists — before an EOIR request arrives. No obligation. No generic answers.